Global natural gas buyers are still signing long-term LNG contracts despite cooling market volatility and lower prices.

But, with liquefied natural gas exporters still looking to ink deals for the massive capacity additions they’re developing through the end of the decade, the terms of contracts this year could portend a continued market shift to affordability over security.

“It’s central to everything right now, as price expectations in the market are moving from what were historically closer to oil parity compared to LNG to pricing that’s closer to coal plus carbon parity,” Columbia University’s Ira Joseph, a global fellow at the Center on Global Energy Policy, told NGI.

That’s not to say that oversupply is likely to push LNG down to cheaper coal parity levels, even with the addition of carbon costs for the dirtier fuel, Joseph added, but the market is headed toward a band of prices that would be critical for establishing a new competitive level for contracts.

A Slippery Slope

Of the deals that have been made this year, Joseph said one of the most significant may be a contract struck between Shell plc and ArcelorMittal Nippon Steel India in May.

While the 10-year contract covered a relatively low volume at 0.5 million metric tons/year (mmty), the parties agreed to a Brent crude-linked slope of 11.5%. It notably became the first oil-linked contract with a slope below 12% since the beginning of the war in Ukraine two years ago.

“This Shell contract is significant because it shows that the market is long on supply in the future, and in order to create the kind of demand growth that will be necessary to clear all of this coming supply, lower prices will probably be needed,” Joseph said.

Shell has been doubling down on its long-term plans for LNG, netting contracts for its massive portfolio of volumes and acquiring more gas assets in Asia.

In February, QatarEnergy disclosed it had signed a 7.5 mmty, 20-year extension with Indian firm Petronet LNG Ltd. Reuters reported the contract was linked at a 12% slope to Brent, indicating QatarEnergy may be lowering its prices to meet the expectations of price sensitive buyers.

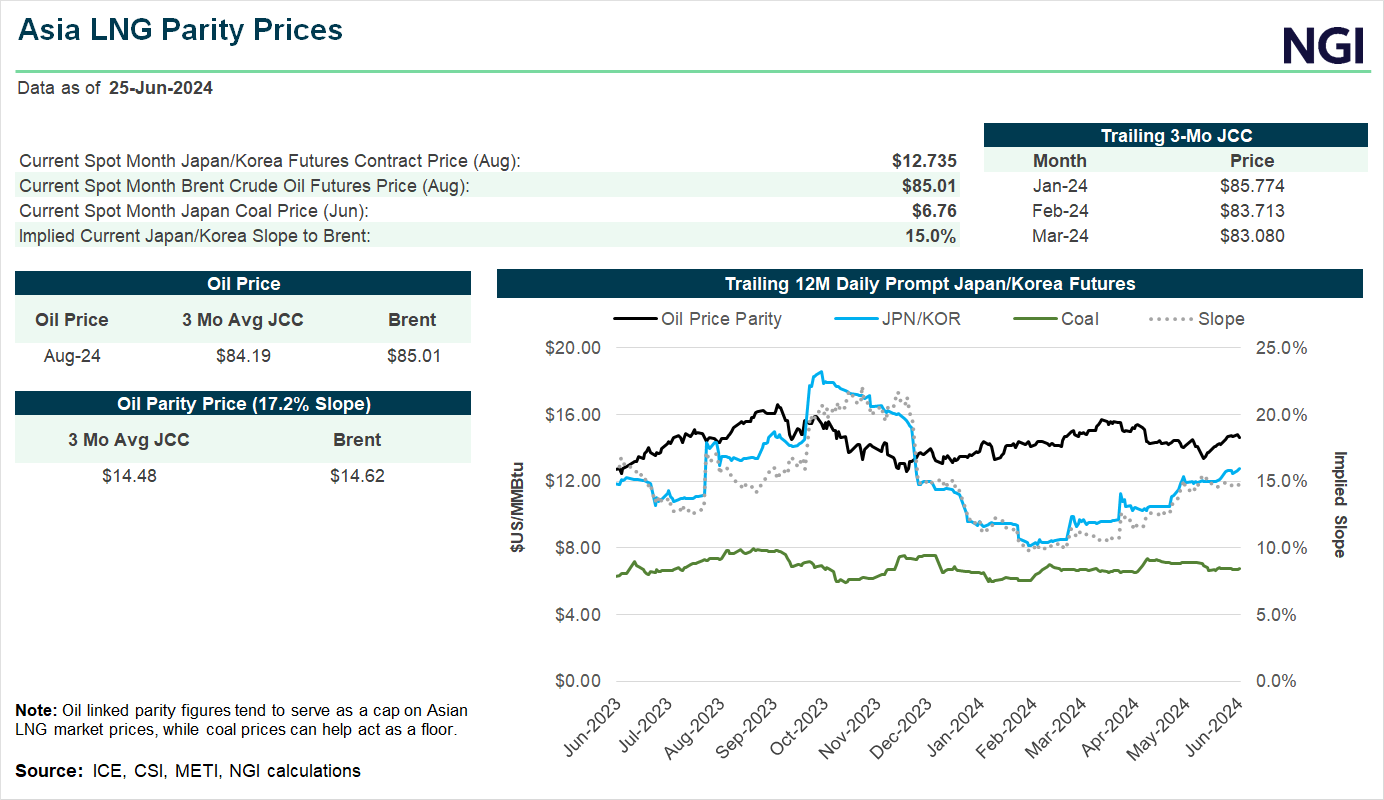

Oil-indexed contracts continue to account for the largest share of LNG supplies in Asia. Brent-linked LNG contracts are typically sold based on an average crude price over the previous three to six months.

August spot contracts for Brent-linked LNG to Asia has hovered above the mid-$14/MMBtu mark for most of June, just slightly higher than the spot Japan Coal Price, according to NGI calculations.

The reduction in demand from European buyers since the beginning of the year and a bevy of available cargoes from the United States has meant that Japan-Korea Marker (JKM) spot prices have been relatively cheaper than crude contracts since late December. Brent-linked spot prices have ranged between $13 to $16, or about a 16-20% slope, since last June.

But, while more volatile during the same period, JKM spot prices have been between $2-6 cheaper than oil-indexed contracts for roughly seven months.

The chance for more oil price volatility, or perhaps persistent oversupply, headed into the end of the decade is also playing into how Asian countries are negotiating with LNG exporters.

The outlook for oil into the latter half of the decade could be in flux, and would largely depend on the effectiveness of global production cuts, according to analysts with Fitch Ratings. However, the market is largely trending toward oversupply.

OPEC+, led by Saudi Arabia, has called for 2.2 million b/d in phased production cuts through September 2025. Since then, some group members have challenged compliance, which combined with forecasts of reduced demand growth, limits the potential for oil price spikes through 2025, according to Fitch.

“This phase-out of cuts, coupled with near-record oil production in the United States and rising inventory levels globally, may move the market into a surplus in 2025,” Fitch analysts wrote.

Everything Must Go

Contract signing has slowed down during the first six months of the year, at least compared to last year. Long-term contracted LNG volumes are expected to rise from 72.7 mmty in 2023 to 112 mmty in 2028 with the addition of deals signed so far this year, according to Bloomberg New Energy Finance data.

In 2023, Qatar and developers in the United States signed a series of long-term contracts as they continued a push to cover export project volumes under development, according to the latest annual report from the International Group of LNG Importers (GIIGNL).

LNG exporters signed 45 long-term contracts last year, which GIIGNL considers to be five or more years. QatarEnergy signed eight 27-year contracts for its various North Field expansion projects. U.S. companies signed a collective 17 long-term agreements during the same period.

Reviewing this year, Joseph said there have been some significant contracts signed, but it is notable that the amount of volumes covered so far in 2024 is relatively small when compared to the amount of proposed capacity still left to sell.

“The Qataris still have probably more than 50 million tons still to sell from the North Field expansion projects, and then over the next 10 years, a lot of their existing contracts are rolling off,” Joseph said.

NGI is currently tracking at least 246.6 mmty in proposed LNG export projects in the United States that haven’t gone to a final investment decision. Another 79.1 mmty is currently under construction, with additional volumes expected to hit the market as soon as the first half of next year.

A partial slowdown in contracting has also been blamed on the U.S. Department of Energy’s pause on new worldwide export permits earlier this year.

In a recent report from the Brookings Institution, however, the think tank wrote that goals to grow investments in net-zero energy infrastructure are keeping key institutional investors from making long-term contract commitments, which is “likely a greater impediment to growing future supply than the LNG pause.”

{kind=link}

{kind=link}

{kind=link}