Natural gas futures treaded lightly throughout Thursday’s session as traders weighed a seasonally weak storage result against continued signs of a pullback among producers.

At A Glance:

- EIA reports 96 Bcf withdrawal

- Output slips below 102 Bcf/d

- Weather demand set to fade

Following a three-day rally, the April Nymex gas futures contract ultimately settled at $1.860/MMBtu on Thursday, down 2.5 cents day/day.

NGI’s Spot Gas National Avg. fell 9.0 cents to $1.480.

Wood Mackenzie estimates showed production just shy of 102 Bcf/d. Output was still up about 2 Bcf/d from a year earlier but down nearly 3 Bcf/d from the prior 30-day average. The decline comes amid vows from some prominent exploration and production (E&P) companies to curtail activity and align supply/demand following a mostly mild winter.

NatGasWeather said the solid heating demand that arrived with a cold front Wednesday in the central United States extended into Thursday as the frigid air pushed to the East and covered a large swath of the Lower 48.

However, the firm added, forecast models maintained a return to benign conditions by the weekend and “strong bearish weather headwinds” through the first half of March “due to little subfreezing air” over most of the country.

“An unseasonably warm versus normal ridge will rapidly strengthen in the days ahead to again rule most of the U.S., with above normal highs of 50s-80s,” the forecaster said Thursday.

Mild conditions have largely dominated the demand side of the natural gas market so far this year. This resulted in another meager storage print Thursday from the U.S. Energy Information Administration (EIA) that helped to keep prices in check.

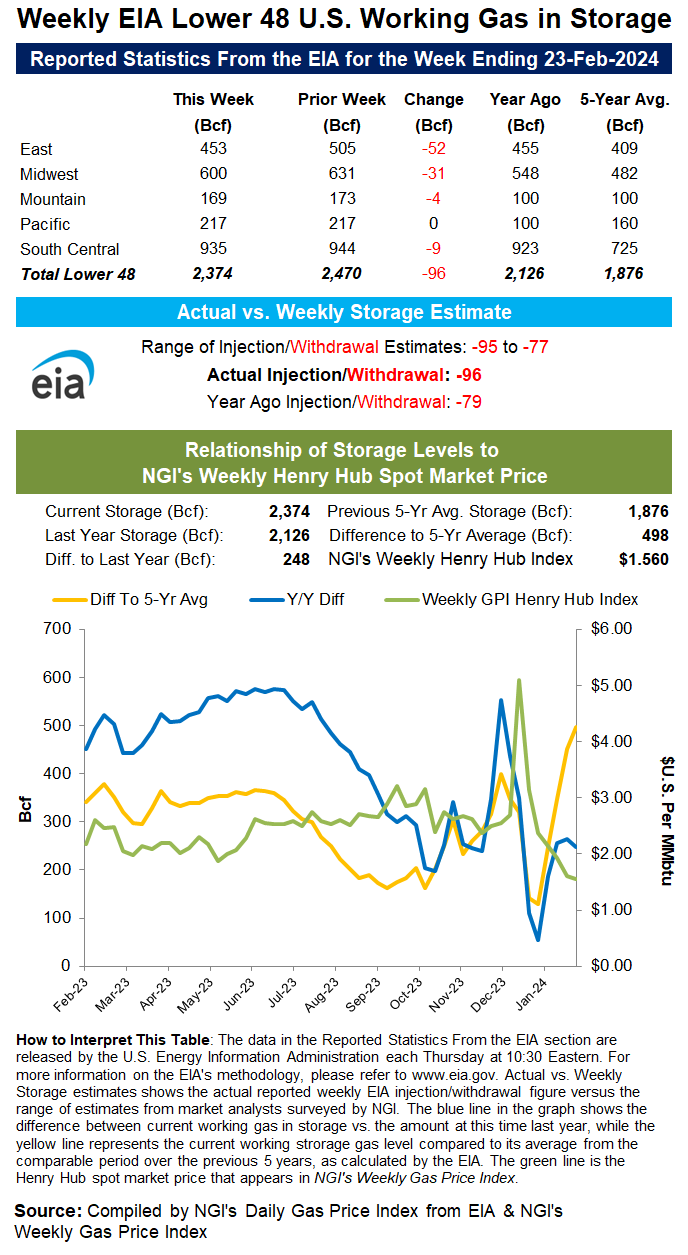

EIA on Thursday reported a withdrawal of 96 Bcf natural gas from storage for the week ended Feb. 23. It was steeper than market expectations for a pull in the high 80s Bcf and briefly boosted Nymex natural gas futures by several cents in morning trading.

However, it paled in comparison to the five-year average decrease of 143 Bcf.

“There was an almost 6.0-cent upside reaction in the 3-4 minutes after” the EIA print. Prices “managed to get back to unchanged and slightly lower on the day fairly quickly as one storage report is probably not enough to get anyone excited for anything big to the upside,” Paragon Global Markets LLC’s Steve Blair, managing director of institutional energy sales, told NGI.

“Production seems to be holding stable over the past week” at levels well below the 2024 peak, and the burst of cold this week provided a bump in demand, Blair added. Still, he said the production outlook is cloudy and recent chilly weather “will be short-lived. And I would expect that demand will not continue to rise.”

Soaring Surplus

The latest inventory print also increased the surplus to the five-year average from 22% to 26.5%. That more than doubled the surplus from the start of the year.

“We are journeying well outside of the five-year range now,” analyst Ryan Parsons of Gelber & Associates said on the online energy platform Enelyst.

Temperatures were warmer than normal over most of the country during the latest EIA report week, “but not as exceptionally so compared to the prior few reports,” NatGasWeather said.

What’s more, the firm added, wind energy generation for the Feb. 23 report period “was nearly 20% stronger” than the prior week, when wind generation was also “quite strong.”

The decrease for last week lowered inventories to 2,374 Bcf, yet stocks were well above the year-earlier level of 2,126 Bcf and the five-year average of 1,876 Bcf.

The East and Midwest regions led with draws of 52 Bcf and 31 Bcf, respectively, according to EIA. The South Central printed a draw of 9 Bcf. Mountain region stocks decreased by 4 Bcf, while Pacific inventories were flat.

Looking ahead to the next EIA report, early estimates submitted to Reuters for the week ending March 1 ranged from withdrawals of 27 Bcf to 54 Bcf, with an average decrease of 34 Bcf. That compares with a pull of 72 Bcf a year earlier and a five-year average decrease of 93 Bcf.

Parsons said while some E&Ps appear to already be easing activity, his firm expects that others will maintain or even increase activity. Permian Basin producers that are cultivating oil – and associated gas, by extension – could even drive an increase in 2024 from last year’s average.

“Despite the cuts in natural gas drilling, overall gas output will still rise in 2024, driven by high crude prices that motivate oil drilling in regions producing substantial associated gas, like the Permian and Bakken Shale,” he said.

Physical Market

Spot gas prices slipped lower Thursday as traders looked ahead to a warm start to March after this week’s brief cold snap.

Northeast hubs led the national average lower. Algonquin Citygate dropped 73.0 cents day/day to average $1.730, and Tenn Zone 6 200L lost 84.5 cents to $1.690.

In the Midwest, Joliet shed 8.0 cents to $1.490, while in the West, SoCal Border Avg. fell 9.0 cents to $1.625.

Prices in West Texas countered the trend, though hubs there were recovering from a temporary supply glut caused by maintenance events. Waha gained 10.5 cents on the day, though it was still far below the national average at 53.0 cents.

Beginning Friday, bulls in the physical market are unlikely to get much help from Mother Nature.

NatGasWeather said while storms were expected to impact parts of the West with rain and light snow over the next several days, “much of the U.S. will warm back above normal” from Friday through next week with highs of 50s-80s for “very light national demand.”

For the second full week of March, the firm said the North would likely experience mild highs of 40s-50s, while southern markets could enjoy springlike highs of 60s to 80s.

Maxar’s Weather Desk on Thursday similarly called for above normal temperatures to cover the eastern half of the Lower 48 throughout the six- to 10-day period, from next Tuesday through Mar. 9.

For days 11 through 15, the updated outlook carried over similar themes of “below normal temperatures at times in the West and mostly steady above to much above normal coverage from the Midwest to the East.”